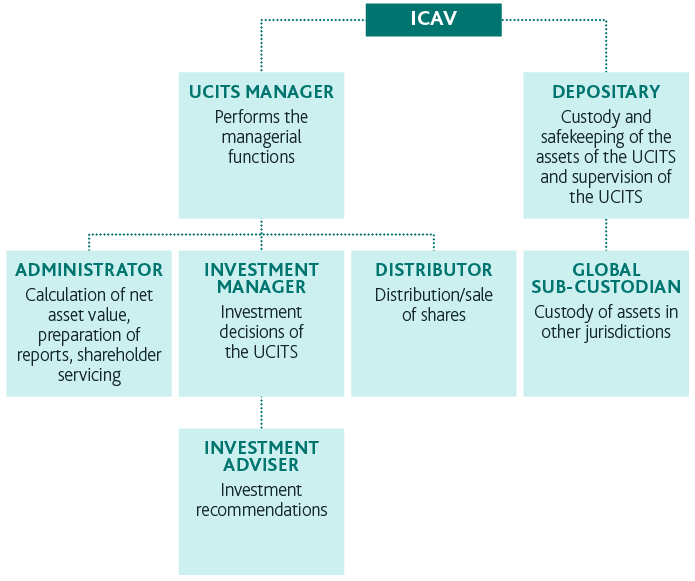

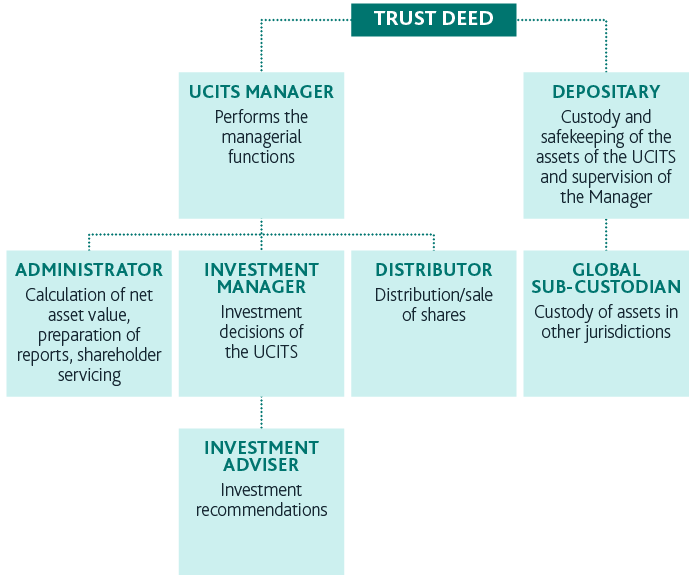

Service providers

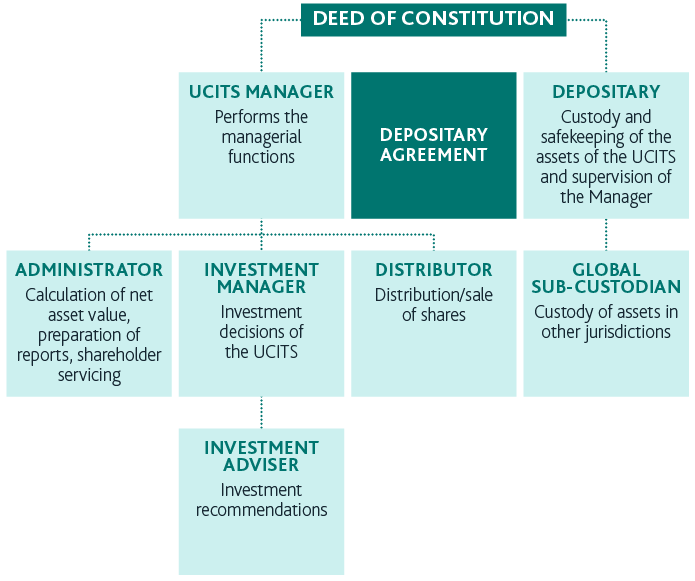

UCITS management company (Manco)

A UCITS Manco will be appointed by the board of the ICAV or the investment company, or in the case of a Unit trust or CCF, it will be the manager to the UCITS fund. A UCITS Manco is responsible for managing UCITS funds. Those functions include investment management, risk management, administration, and marketing. It is possible for a UCITS Manco to delegate some or many of these functions, provided it retains sufficient substance for its operations in Ireland and maintains a minimum headcount of at least four full time employees or equivalent, so that it is not considered to be a so-called “letter-box entity”.

A UCITS Manco is required to adopt a business plan setting out its organisational structure, the responsibilities of its senior management, and information on how it intends to comply with its obligations under Irish law. Under a business plan, the UCITS Manco is responsible for the following key designated managerial functions:

- regulatory compliance;

- fund risk management;

- ·operational risk management;

- investment management;

- capital and financial management;

- distribution.

A UCITS Manco must have designated persons who are responsible for the above managerial functions. The designated person responsible for the investment management function is not permitted to also be responsible for the fund risk management function or operational risk management function. Designated persons can be an employee of the UCITS Manco. Alternatively, a suitably qualified person can be seconded to act as designated person on behalf of the UCITS Manco.

Investment manager

Sometimes the UCITS Manco will not assume responsibility for the discretionary management of the UCITS fund’s investments and therefore it is necessary to appoint an investment manager that will undertake responsibility for discretionary portfolio management. The function of the investment manager is to undertake day-to-day investment decision making on behalf of the UCITS fund.

The UCITS Directive provides that only investment firms that are authorised for the purpose of asset management, and which are subject to prudential supervision under a regulatory regime that is broadly equivalent to EU standards, may be appointed to act as a discretionary investment manager of UCITS funds. Accordingly, European authorised investment managers that meet certain requirements – for example, that are authorised under the MiFID Directive – are not subject to an approval process.

The Central Bank will, however, require confirmation from the home state regulator that the investment manager has the appropriate regulatory status.

Where the UCITS fund proposes to delegate discretionary investment management to an investment firm based in a third country, cooperation between the Central Bank and the supervisory authority of the investment firm must be ensured. The Central Bank has accepted several jurisdictions as having a comparable regulatory regime. They include: Abu Dhabi; Australia; Bahamas; Bermuda; Brazil; Canada; Dubai; Guernsey; Hong Kong; India; Japan; Jersey; Malaysia; Qatar; Singapore; South Africa; South Korea; Switzerland; and the US.

The Central Bank will apply an approval process to ensure that the investment firm is subject to regulation and ongoing prudential supervision that is equivalent to EU standards. The Central Bank’s approval process requires the completion of an application form by the prospective investment manager and requires the filing of the investment manager’s audited accounts.

Depositary

The depositary is responsible for holding and safekeeping the assets of a UCITS fund. Strict obligations are imposed on the depositary relating to monitoring cash flow, safekeeping of assets and detailed oversight, verification, and monitoring obligations.

The depositary is also subject to strict liability for loss of a financial instrument held in custody, unless proven that the loss arose by virtue of an external event beyond the depositary’s reasonable control. This strict liability affords investors in a UCITS fund a strong level of protection. The depositary is also liable to the UCITS fund and its investors for all losses suffered due to the negligence or intentional failure by the depositary to properly fulfil its obligations under the UCITS Regulations.

In addition, there are stringent rules regarding delegation and the depositary must comply with minimum ongoing monitoring requirements for any delegates.

Administrator

An administrator, which is authorised by the Central Bank to conduct administration activities, must be appointed to provide administration services to an Irish authorised UCITS fund. The Central Bank imposes rules on the outsourcing of administration activities, intended to promote greater consistency and certainty. While the outsourcing of certain activities is permitted, “core administration activities” such as the final checking and release of the net asset value per unit/share, as well as the maintenance of the shareholder register, cannot be outsourced.

Directors

An ICAV, an investment company or a UCITS Manco must have at least two Irish resident directors, which are required to be pre-approved by the Central Bank. All directors need to comply with the Central Bank’s fitness and probity requirements (the F&P requirements).

The F&P Requirements require the collation of certain due diligence for each director and the filing of an individual questionnaire (IQ) with the Central Bank. The F&P requirements allow the Central Bank to satisfy itself that the proposed directors are: competent and capable; honest, ethical and will act with integrity; and financially sound.

The time it takes to nominate suitable directors and obtain their approval is a process that can take weeks to complete and should be considered as part of the authorisation timetable.

Taxation of UCITS funds

Fund level taxes

UCITS funds are subject to Ireland’s favourable tax regime for investment funds. In particular, UCITS funds are exempt from Irish tax on income and gains derived from their investment portfolios and are not subject to any Irish tax on their net asset value. UCITS funds do not charge any withholding taxes on payments to investors, and no stamp or capital duty is payable in Ireland on the issue, transfer, repurchase, or redemption of units/shares in a UCITS fund.

No withholding taxes

No Irish withholding taxes apply to the payment of dividends or distributions to investors who are not resident in Ireland and have provided the UCITS fund with the appropriate tax residence declaration. The payment of redemption proceeds, returns of capital or payments in relation to the encashment, cancellation, or transfer of units to non-Irish resident investors, are also exempt from Irish withholding taxes.

Stamp duty and subscription taxes

No stamp duty is payable in Ireland on the issue, transfer, repurchase or redemption of shares in a UCITS fund. No subscription taxes are levied by the Irish tax authorities on the assets of a UCITS fund.

Treaty access

Ireland has an extensive network of double taxation treaties and the Irish tax authorities consider that UCITS funds, other than CCFs, are generally entitled to the benefit of Ireland’s extensive tax treaty network. The availability of treaty benefits may enable a UCITS fund to avail of reduced rates of foreign withholding tax that would otherwise apply to the holding of foreign assets. Tax treaty access can be restricted depending on the provisions of relevant tax treaty and the approach of the tax authorities in the treaty country where the UCITS investments are located.

Election for US tax purposes

A UCITS fund that is established as an ICAV can elect to ‘check-the-box,’ which under US tax regulation operates to classify the ICAV as a partnership or a disregarded entity for US federal tax purposes. This feature can enhance the attractiveness of the ICAV for US taxable investors, who generally prefer to invest in tax transparent vehicles. An ICAV is subject to the same domestic tax treatment as other corporate funds – i.e. there is no Irish tax on its income or gains, and no Irish withholding taxes or stamp duty applies.

VAT

The provision of certain standard services to Irish UCITS funds, such as investment management, administration, transfer agency and depositary services, are treated as VAT exempt in Ireland. Other services, such as legal and accounting services, can result in a liability for Irish VAT. UCITS funds can, however, recover such VAT charges based on the VAT recovery rate, which is calculated on the proportion of the UCITS fund’s investments located outside the EU, or alternatively based on the portion of investors that are located outside the EU.

Distribution

UCITS funds benefit from a harmonised legal framework whereby a UCITS fund that is established in Ireland can, following the completion of a notification procedure, be sold cross border in another EEA member state without the need for additional authorisation. Furthermore, UCITS funds are often recognised by regulators in markets in the Middle East, Latin America, and Asia.

The procedure for the notification of the marketing of a UCITS fund in another jurisdiction is relatively straightforward and requires the UCITS fund to submit a standard notification together with supporting documentation to the Central Bank.

Once a complete notification is received, the Central Bank will review the notification, and if it is satisfied with all the documents, they will forward this notification to the host state regulator within 10 working days.

Usually, marketing of the UCITS fund can commence immediately following receipt of the confirmation from the Central Bank that it has transmitted the notification to the host state regulator. Under the UCITS regulations, EU member states are prohibited from imposing additional requirements and it is only the key investor information document (KIID) that is required to be translated, which is a change from the previous requirements that had resulted in costly translation expenses.

The UCITS fund has been hugely successful since its inception and has developed into a global brand that has strong market penetration in jurisdictions outside of the EU. The procedure for distributing UCITS funds outside of the EEA is country specific and distribution needs to be considered on a jurisdiction-by-jurisdiction basis.

However, due to the high level of investor protection afforded by UCITS funds, typically, UCITS funds are treated as regulated retail funds for the purposes of registration in jurisdictions outside the EEA – indeed, some jurisdictions outside of the EU have a specific ‘fast-track’ approval process for UCITS funds. UCITS funds can be registered for public distribution in non-EU jurisdictions, such as Switzerland, Singapore, Hong Kong, Macau, Taiwan, Chile, Peru, South Africa, and Bahrain, where UCITS funds have developed strong brand awareness and market recognition.

To date UCITS funds are distributed to over 90 countries worldwide.

Regulatory approval process and timeframe

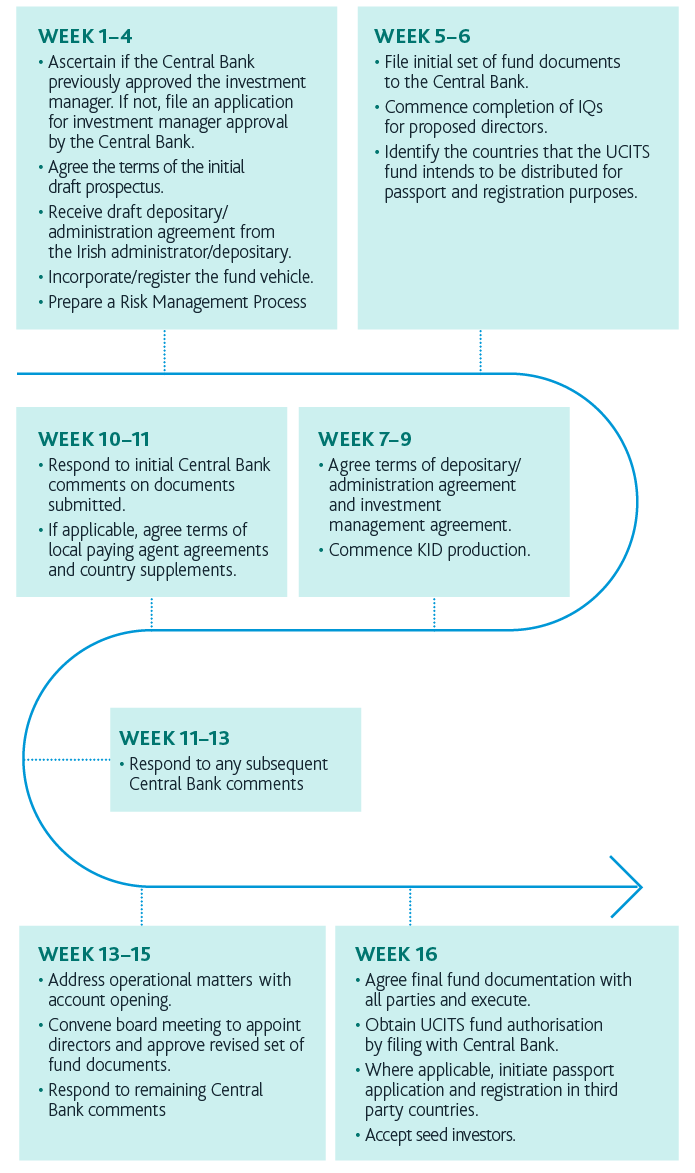

Depending on its nature and complexity, we normally advise that a realistic timeframe for the authorisation of a UCITS fund is a period of between 12 to 16 weeks from the date we are requested to commence the initial filing with the Central Bank.

The procedure for the authorisation of a UCITS fund involves obtaining the Central Bank’s approval of the directors and the investment manager of the UCITS fund, as well completing the Central Bank’s review and approval of core fund documents, primarily the prospectus.

The review and approval of the core fund documents commences with an initial application being filed with the Central Bank. The Central Bank has 20 working days from the date of the submission of this application to issue its comments. Once those comments are received and responded to, the Central Bank has 10 working days to review the responses and issue any additional comments. This review and comments process will continue until the Central Bank confirms that it has no further comments. At that point, the application for authorisation of the UCITS fund can be submitted to the Central Bank.

There are many other documents, such as investment management agreement, administration agreement, depositary agreement, distribution agreement, and letters of confirmation, among others, that need to be filed with the Central Bank for authorisation purposes. For these documents, the Central Bank requires the UCITS fund’s legal advisers to certify compliance with the UCITS Regulations, and these documents are filed with the Central Bank immediately prior to authorisation of the UCITS fund.